India still loves FDs!

Dear Investor,

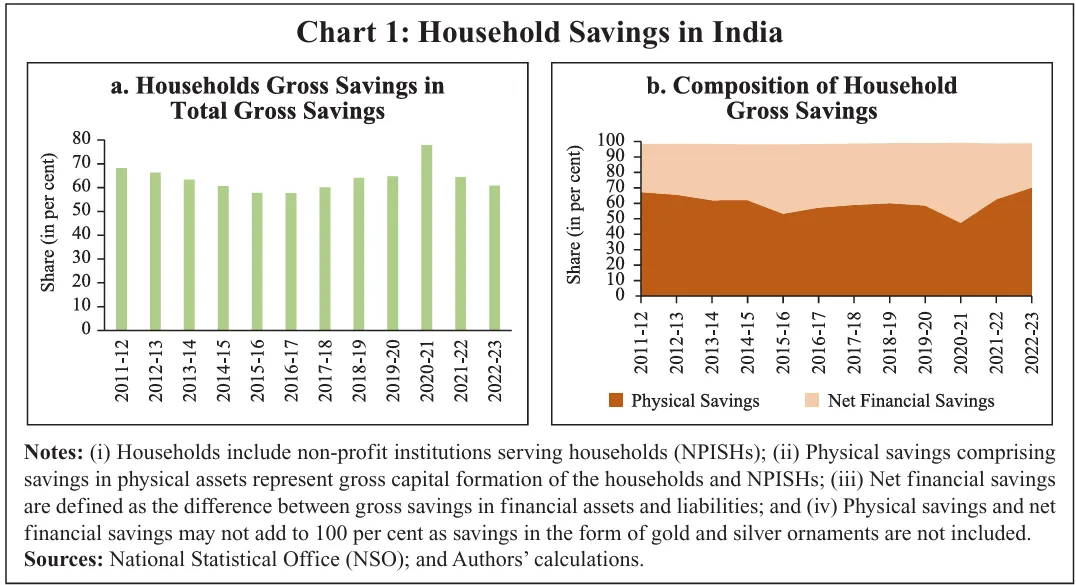

It’s well known that Indians have historically preferred safe and traditional investments to safeguard their wealth. This is evident even today, with a huge share of Indian households’ savings (~90%) in physical assets like real estate.

Similarly, when it comes to financial instruments, FDs have reigned king. But while this remains true even today, alternate assets like stocks and mutual funds are rapidly gaining market share thanks to increasing financial literacy.

Increasing financial literacy and portfolio diversification? Sounds great, doesn’t it? Well, maybe not.

As per a recent

RBI study

on household investment decisions, the move towards alternate assets may not be as well thought out as it seems.

“What’s wrong with the move towards alternate assets?”

While a move towards more sophisticated financial instruments can generally be seen as a positive sign, the reason for the move is just as important. Some of these reasons are explored in the RBI publication titled Determinants of Household Saving Portfolio in India: Evidence from Survey Data.

The study is quite detailed and covers many aspects of what goes into household investment decisions. We will not be delving into the technicalities today, and will just focus on one of the conclusions of the study:

“Of the three types of returns on instruments considered in the paper, interest rate on term deposits positively influences saving decision in assets like fixed deposits and post office savings, while house prices have a mixed impact across rural and urban areas on savings in financial assets.

Stock market returns have a statistically insignificant relationship with the investment decisions in equity and mutual funds.“

Understandably, people invest more in FDs when returns are higher. But this is not the case with equity and mutual funds!

This is quite a worrying conclusion. Think about it, investment decisions in equity and mutual funds seem to have no correlation with the returns they offer!

(On that note, FDs are at a decade-high, offering as much as 9.1% p.a.)

“So how do people allocate funds towards these assets?”

The primary considerations for investments should be risk and returns. But many secondary and tertiary factors go into investment decisions, sometimes even sidelining the primary factors.

For example, stock market investments offer higher returns, diversification options, higher liquidity, and other objective benefits over traditional investment avenues. Additionally,

psychological biases and social conditioning

also contribute to increasing stock market participation.With so many factors to consider, investors may downplay the fundamental consideration - risks v/s returns, resulting in seemingly irrational behaviour.

“How can I avoid these mistakes when investing?”

(We’re not investment advisors, so maybe take this with a pinch of salt.)

It’s simple, make investing as mathematical as possible. If you can quantify every factor you consider, it will significantly decreases the odds of making irrational decisions. Estimate your risk tolerance, set financial goals, and use that as the basis to make a solid investment plan.

And always keep the fundamental factor in mind, it’s risks v/s returns.

As you continue your investing, regularly rebalance your portfolio to maintain your desired asset allocation and manage risk.

As we’ve seen today, many factors go into making investment decisions. And you need to make sure you don’t end up making irrational decisions as a result.

We’ll be sure to keep you informed with such deep dives into the financial system.

Until next time, have fun Super Investing!

You can book

mathematically optimal, RBI-insured FDs

on our platform. Up to 9.1% p.a. interest rates and ₹5L insurance from the DICGC.Disclaimer: This content is meant purely for educational purposes and is not to be taken as an investment advisory.