Indian banks dominate the long-term FD market!

Dear Investor,

Foreign banks today hold about 5% of the total bank deposits in India. And that’s not really surprising, given that people tend to choose their banking partners based on trust. (Not to say that foreign banks are not trusted, just that it’s easier to trust a bank that you know is based in your own country.)

What is surprising is how their deposit portfolio differs from domestic banks. A significant portion of deposits with foreign banks is parked in shorter-term FDs and savings accounts, in sharp contrast to deposits with Indian banks.

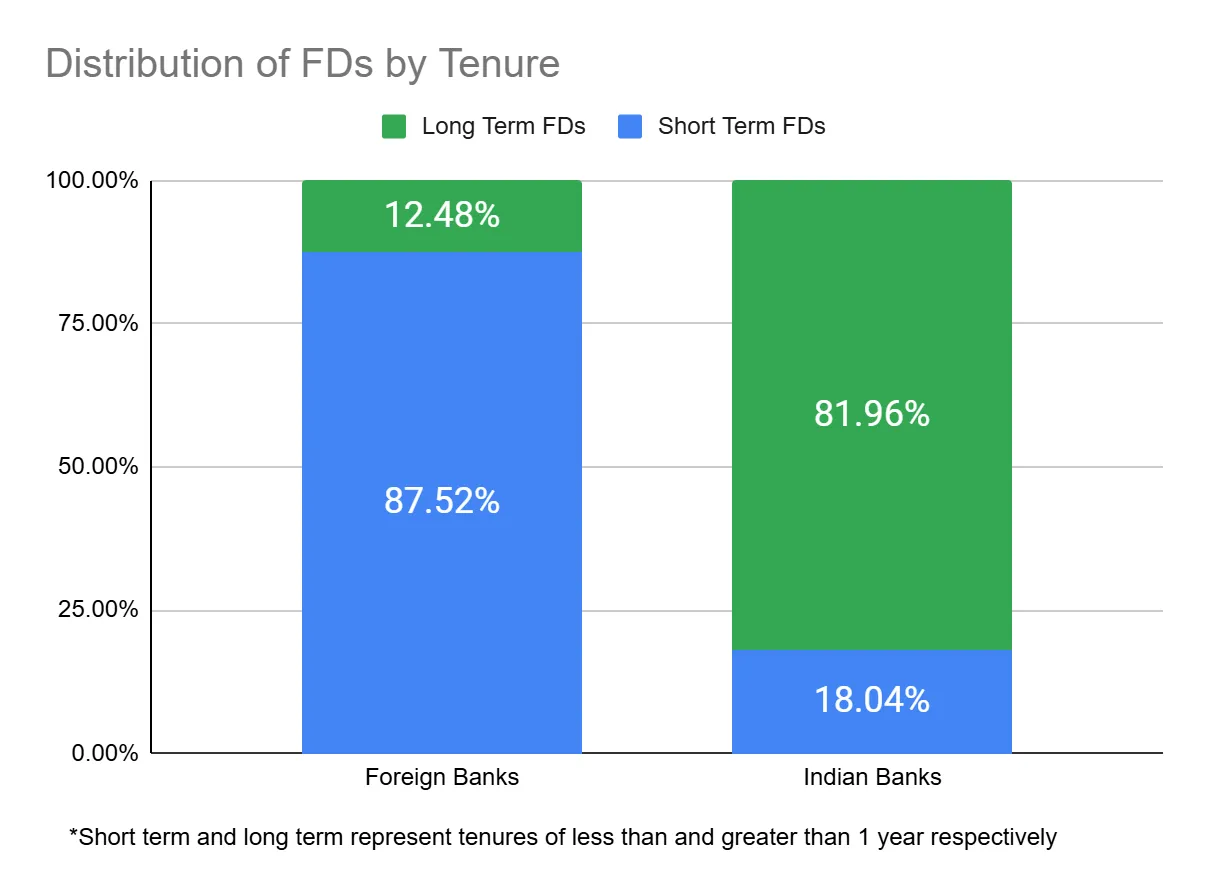

The difference is massive. As much as 87.5% of FDs with foreign banks have tenures of less than 1 year. For Indian banks, that number is just over 18%.

“So what if people prefer short-term FDs in foreign banks? Why should I care?”

Before we get into that, we need to look at the breakdown of foreign bank FDs in more detail. Think the 87.5% was shocking? Over 60% of foreign bank FDs have tenures of

less than 91 days.

Another 16.8% have tenures less than 6 months.(Data as per RBI records)

So it’s not just short-term, it’s ultra short-term. And 5% of the total deposit market? It adds up to about

₹

6 Lakh Crore.Curious now?

“Ok, why do people prefer short-term FDs in foreign banks?”

Foreign banks tend to adjust their interest rates more frequently in response to global market conditions and RBI policies. And since they are more sensitive to changes, the banks themselves prefer to have shorter term commitments.

This means that while right now, foreign banks may not offer the highest short-term FD rates, it’s possible that they did in the recent past or will in the near future.

So while it may seem that Indian banks and foreign banks are offering the same product to the same audience, their business outlooks are different.

Foreign banks don’t want to lock-in prevailing rates, so they offer better rates on short-term deposits. They also change rates more often to keep up with the market conditions.

Domestic banks do want to lock-in long-term capital, so they offer better rates on long-term deposits. They also tend to change rates only in response to bigger market movements.

(Data as per RBI records, excluding RRBs)

Neither one is better or worse, they’re just different strategies.

With all this in mind, you can think of short-term FDs and long-term FDs as somewhat independent products, and rate changes is one do not always indicate changes in the other’s.

As we’ve seen today, even similar businesses may have completely different strategies, targeting different segments of the market. And also, short-term deposits in foreign banks are a useful avenue to diversify your portfolio over different time horizons.

We’ll be sure to keep you informed with such deep dives into the financial system.

Until next time, have fun Super Investing!

Disclaimer: This content is meant purely for educational purposes and is not to be taken as an investment advisory.