Tired of hearing about the ₹12L tax exemption?

Dear Investor,

The recent changes to the tax structure announced in the Union Budget 2025-26 has certainly got everyone excited. The increase in tax exemption from ₹7L to ₹12L will have many interesting effects on the economy.

But we’re sure you’ve heard enough of it. We’re here to explain some less obvious aspects of the additional ₹5L exemption - on your investing decisions.

“How will this change anything about my investments?”

Let’s take an example of someone making ₹10L in salaried income annually. Earlier, ₹7L would be tax exempt and any investment gains would be taxed normally. Under the new system, however, the entire ₹10L is tax exempt, and there’s still an extra ₹2L of potential income that could be tax free.

Here’s where things get interesting: not all investment instruments qualify under this exemption. Capital gains from stocks, mutual funds, and property sales are still taxable: LTCG at 12.5% and STCG at slab rates.

Note - ₹60,000 rebate is not applicable on STCG.

However, interest earned on Fixed Deposits (FDs) and savings accounts falls under taxable income—meaning it can now be covered by the ₹12L exemption.

“What should I do differently?”

If you’ve been prioritizing riskier equity investments for tax efficiency, it might be time to reconsider. With the new rules, a balanced approach, including fixed-income instruments, could yield better post-tax returns.

With FD interests now falling under the exemption limit, this traditional investment become more attractive. Previously, taxes would eat into the FD returns, but now, up to ₹12L total income, those returns remain untouched. You read it right. Now, you can even earn 9.5% p.a. post tax return on FDs!

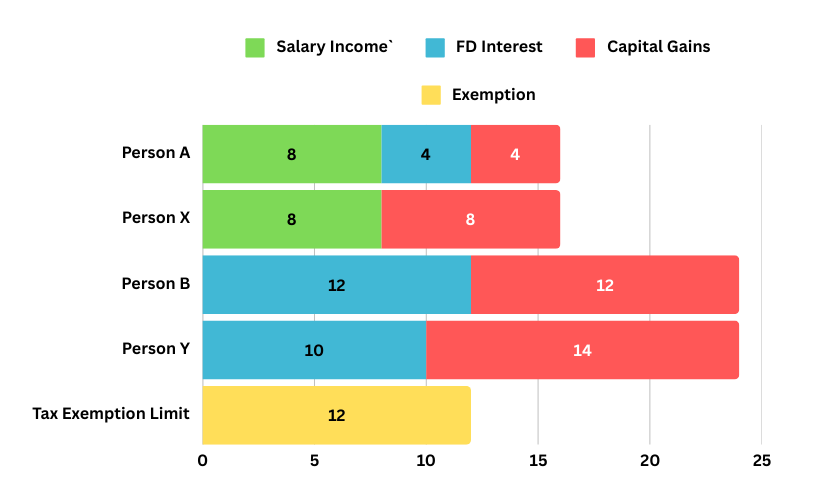

Persons A and B are making use of the entirety of tax exemption available under the new system.

Persons X and Y are missing out on potential tax exemption by focusing too much on capital gains over fixed interest products. In spite of having similar incomes as A and B, more of their income is taxed.

“What if my primary income is through investments?”

This change benefits those who rely on passive income sources like interest earnings. Especially for those who are close to retirement or retired - As Deepak Shenoy, Capital Mind, quotes - “FD becomes the preferred investment choice for the first ₹2 Cr of your retirement fund”.

It’s time to help your parents with the best retirement fund strategy.

While it’s tempting to focus on the headline tax exemption, the real advantage lies in how you adjust your investments accordingly. A more informed strategy could help you make the most of this tax structure change.

Our honourable Finance Minister is making FDs Super! Do check out Super FD for 9%+ FD returns.

We’ll be sure to keep you informed with such deep dives into the financial system.

Until next time, have fun Super Investing!

Disclaimer: This content is meant purely for educational purposes and is not to be taken as an investment advisory.